Insights

The Federal Government has announced significant changes to the proposed Division 296 tax under its Better Targeted Superannuation Concessions (BTSC) for individuals with high-balance accounts. The updates are in response to industry and stakeholder feedback and are believed to be more practical than the previously proposed legislation.

What’s changed?

1. A two-tiered approach to additional taxes

Tiered tax rates are now proposed, with a new higher threshold and an increased tax rate applying. For members with a total superannuation balance (TSB) over the relevant tiers, additional tax will apply to the member’s share of fund taxable income based on the proportion of their balance over the relevant tiers/thresholds:

| Total superannuation balance (TSB) | Tax rate |

| Up to $3m | 15% in the super fund (unchanged) |

| $3m – $10m | 30% (15% in the super fund and 15% levied on the member) |

| Over $10m | 40% (15% in the super fund and 25% levied on the member) |

2. Indexation of the balance thresholds of $3m and $10m

Both thresholds will be indexed to CPI/inflation in alignment with the Transfer Balance Cap. This will reduce the number of individuals affected by the measure over time when compared to the previous proposal, where the $3million threshold was not indexed.

The $3million threshold will increase in increments of $150,000, and the $10million threshold will increase in increments of $500,000.

3. Unrealised gains no longer taxed

One of the most significant changes is the removal of the proposal to tax unrealised capital gains. This addresses major concerns raised by SMSF holders and investors, ensuring that only realised gains will be subject to the new tax e.g., gains from assets sold. However, there remains uncertainty as to how these new measures will accurately capture capital gains realised from the proposed start date only without the inclusion of gains accrued up to that date.

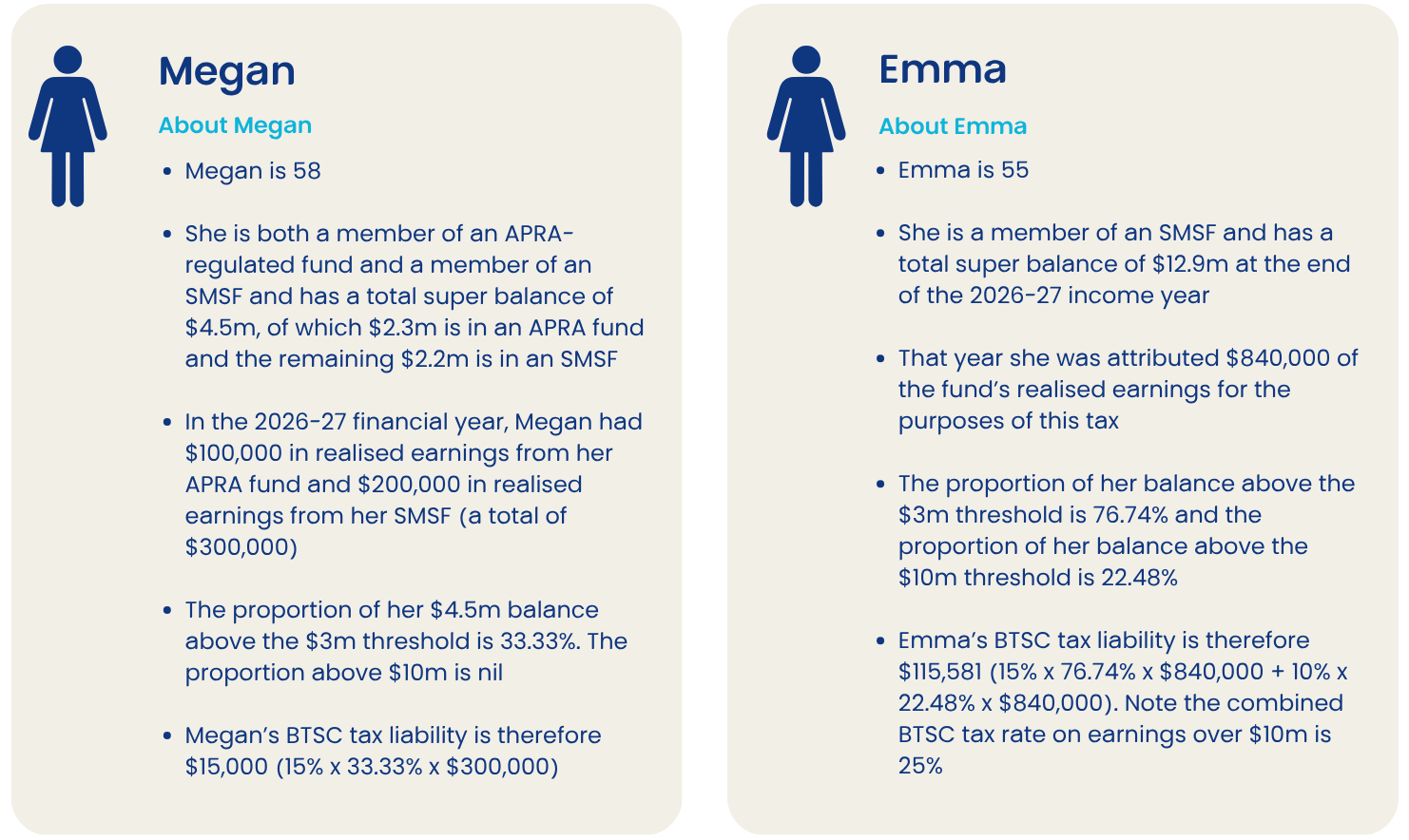

Examples

When will the legislation be implemented?

The proposed start date for the revised measure has been pushed back to 1 July 2026 with the first Division 296 tax assessments in respect of the 2026-27 financial year being issued in 2027-28. This allows time for consultation on the final legislation.

What should you do next?

Super fund members should wait until legislation has passed before considering any action. There are still many questions to be answered in relation to the proposed legislation. The Government intends to release draft legislation for industry consultation before the proposed measures are implemented.

More information can be found here.

If you have questions about how this impacts you and your superannuation, please get in touch.

22 Oct 2025

Related insights

Insights

The Federal Government has introduced major changes to superannuation guarantee rules. The Payday Super legislation, which received Royal Assent on 6 November 2025, will take effect from 1 July 2026.Key changesFrom 1 July 2026, employers must ensure superannuation contributions are paid into their employee’s nominated fund within seven business days...

2 contributors

Perth

Insights

Whether you're buying a business, selling a business, or raising capital in Australia, each pathway comes with its own technical processes and risks. Our comprehensive guide to mergers & acquisitions and capital raising highlights the critical steps, risks, and tax considerations you need to know.The guide covers: The strategic importance...

2 contributors

Perth

Insights

The PKF Perth team is proud to have acted as financial and tax adviser to the shareholders of Dataline Visual Link Pty (DVL) in the sale of the business to ASX-listed Intelligent Monitoring Group (IMG). DVL is a Perth based provider of high-quality and leading-edge electronic security solutions, including CCTV...

Matthew Hall

Executive Director

Perth