Insights

AASB 18 Presentation and Disclosure in Financial Statements is the next big accounting standard that will affect most entities who prepare general purpose financial statements.

What do you need to know now?

Whilst this standard is receiving some media attention regarding the changes, it is important to understand who and when this applies to entities within Australia since the transition to this standard is confusing with some unknowns.

Background to the change

AASB 18 is the international equivalent to IFRS 18 issued by the International Accounting Standards Board (IASB) and in line with government policy, the AASB has issued this standard in Australia. However, while the audience of the IASB standards is publicly listed entities, the AASBs are applicable to each sector in Australia, public and private sector, for-profit and not-for-profit.

AASB 18 will replace the current AASB 101 Presentation of Financial Statements.

This new standard focuses on enhancing the clarity and comparability of primary financial statements, aiming to provide more useful information to investors and other stakeholders.

AASB 18 does not change recognition or measurement principles, rather it deals with presentation and disclosure principally related to the primary statements and therefore reported profit, revenue, assets and liabilities will not change.

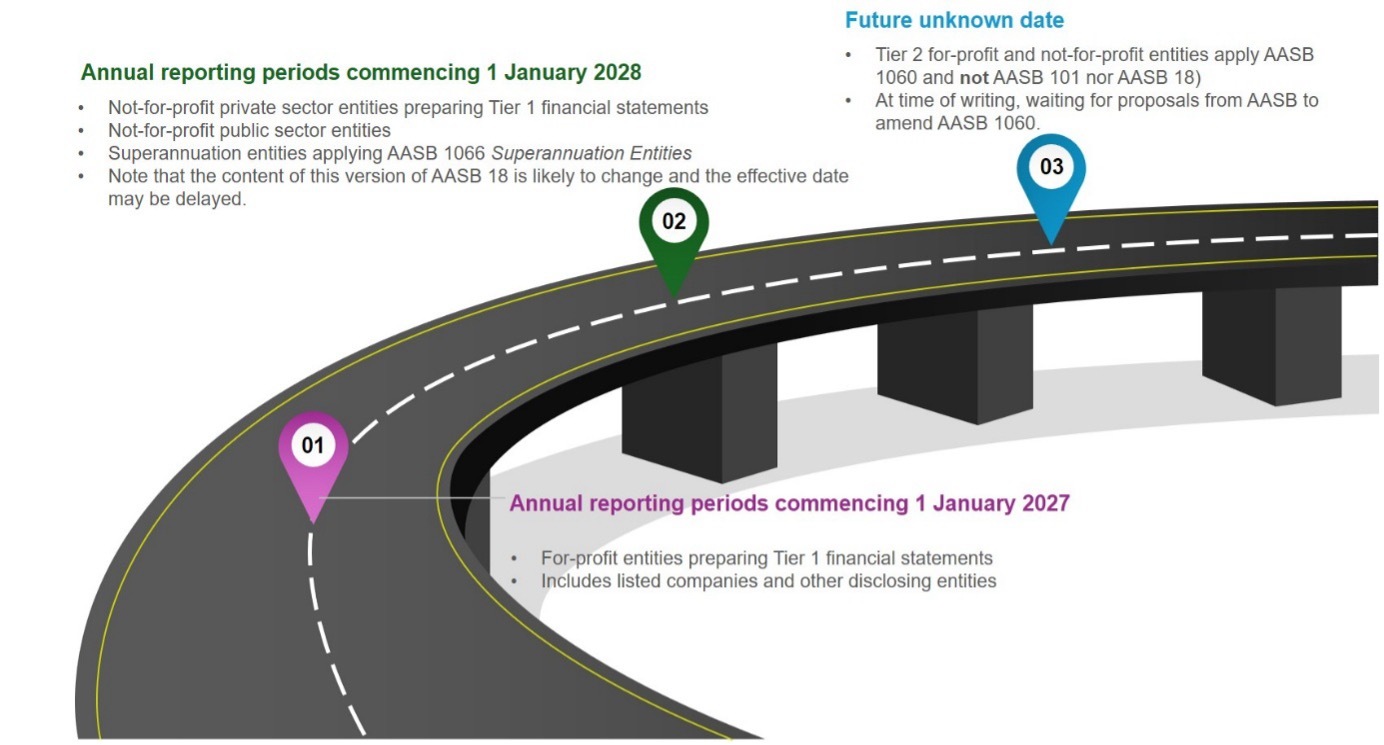

Scope and timing of AASB 18

Before we get into the detail of the changes, it is important to understand in Australia the timing and availability of AASB 18 depends on the type of entity as illustrated in the roadmap below:

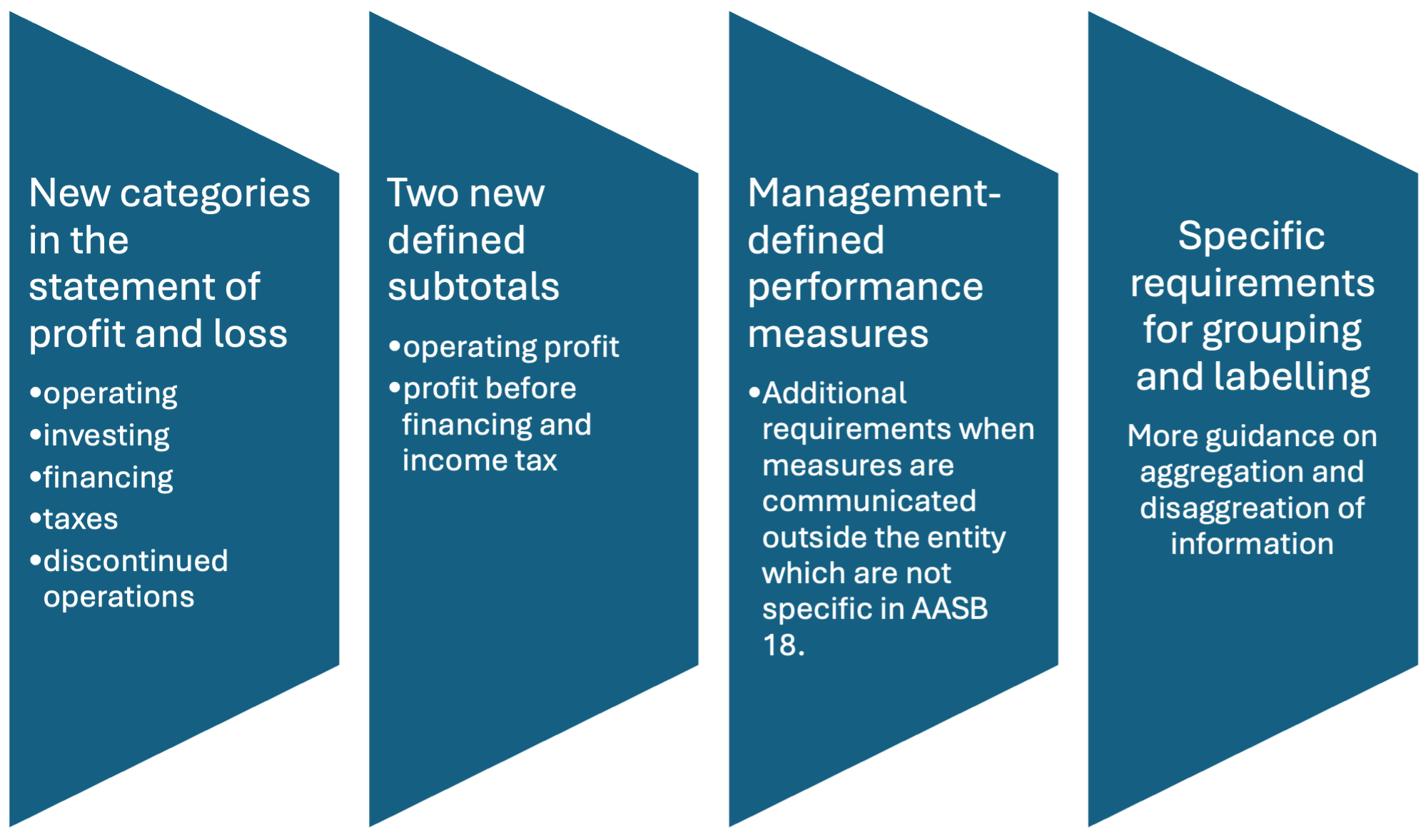

Key Changes Introduced by AASB 18

The key changes are highlighted in the diagram below and discussed further in the following sections.

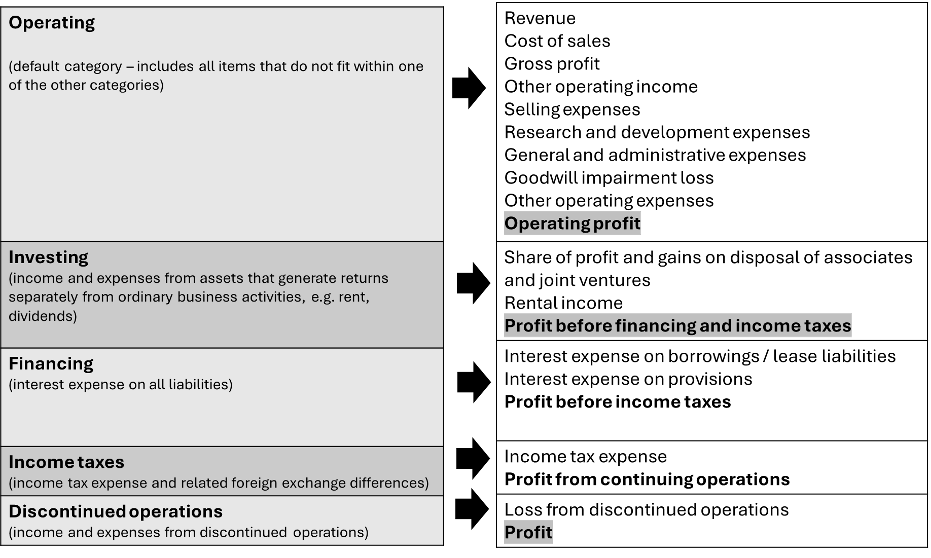

New categories in the statement of profit and loss

To facilitate comparability and consistency, the statement of profit and loss will now be split into five categories. Note that the other comprehensive income section is still required but has not been illustrated below.

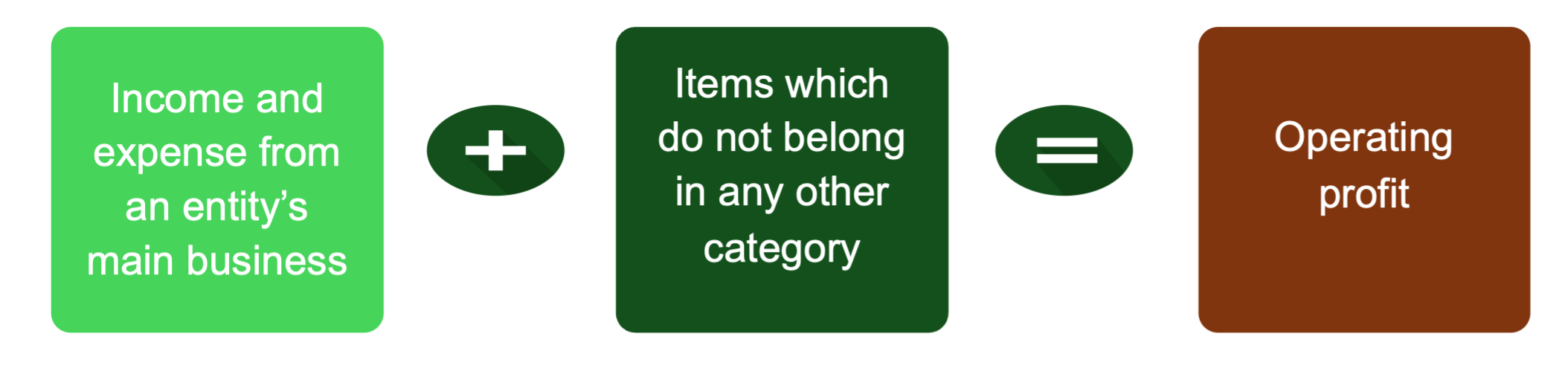

The shaded sub-totals are those required by AASB 18 as well as total other comprehensive income and total comprehensive income.The operating category are those items which do not fit into any of the other categories and therefore this is therefore the default category.

The illustration above is for entities who do not have specified business activities, AASB 18 has different presentation requirements for certain entities who providing funding or invest in certain assets, i.e. a bank would show interest transactions as operating rather than investing or financing.

These new categories will require entities to carefully consider their current chart of accounts and mapping to the financial statements since the classification under AASB 18 may require much more granular information than currently reported as well as documented positions on why certain income and expenses have been included in particular sections.

Two new defined subtotals

AASB 18 introduces two new mandatory subtotals for the statement of profit and loss to provide a consistent base for analysis of entity performance.

Operating profit and profit before financing and income taxes will now be included on the primary statement for all entity financial statements.

Operating profit is comprised of:

Entities should consider whether they currently use operating profit for metrics such as management incentives or bank covenants since AASB 18 could cause confusion if the calculation is based on different numbers.

Profit before financing and income taxes is equal to operating profit plus/minus the transactions included in the financing section of the statement of profit or loss.

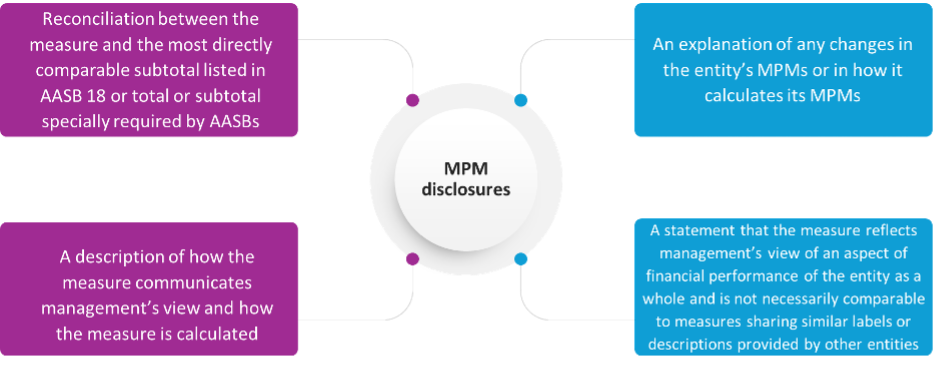

Management-defined performance measures

These requirements are to provide more rigour around the performance measures used by entities to explain their performance which are supplementary to the information required by the accounting standards.

There are three criteria which need to be met for a metric to be a management-defined performance measure (MPM) under AASB 18:

- The metric is a sub-total of income and expenses not required or specifically exempted by AASBs.

- The metric has been used in public communication outside the financial statements.

- The metric is used to communicate management's view of an entity’s financial performance.

Since the first criterion involves a sub-total of income and expenses then metrics such as free cash flow, net debt, customer satisfaction or revenue growth will not meet the definition of an MPM.

Once an MPM has been identified by management, there are additional disclosures needed in the notes to the financial statements:

Since these disclosures will be included in the financial statements, they are required to be audited.

Specific requirements for grouping and labelling

AASB 18 provides additional guidance on which transactions should be grouped together (aggregated) and disclosed separately (disaggregated) which will need to be considered by entities in determining line items in the primary financial statements and the notes.

In addition, AASB 18 clarifies that the primary financial statements provide a structured summary of an entity’s income, expenses, assets, liabilities and equity, while the notes provide additional material information necessary for users to understand the amounts presented in those statements. Accordingly, the notes should not simply repeat information already presented in the primary financial statements. This clarification should support the removal of unnecessary duplication and help entities declutter their financial statements, consistent with the principle that material information should not be obscured by immaterial information.

A welcome change for many entities will be the ability to present expenses by both nature and/or function where this provides the most useful structured summary.

Other points of note

Whilst there are some substantial changes to presentation and disclosures within the financial statements under AASB 18, many of the fundamental concepts that we know from AASB 101 will remain in place.

This includes:

- Materiality

- Consistency

- Going concern

- Current / non-current classifications and definitions and

- Material accounting policy information.

On adoption of AASB 18, there will be some consequential amendments to other standards, including AASB 107 Statement of Cashflows where the presentation alternatives for interest and dividend cash flows have been removed for most entities. Dividends and interest paid will generally be classified in cash flows from financing activities, and dividends and interest received will generally be classified in cash flows from investing activities.

For further information on any of these changes, please contact your nearest PKF office.

9 July 2026

Related insights

Insights

Over the past year, PKF, working with the Governance Institute of Australia, Macquarie University’s DataX Research Centre, and other expert organisations, has supported an important research study to assess the data governance landscape in Australia. The findings are unexpected and motivating.Survey participants and process In August 2023, the Governance Institute...

Ken Weldin

Partner

Melbourne

Insights

AI’s enabling power spans diverse applications and fields. Unlike traditional technologies, AI possesses the ability to learn, adapt, and perform tasks that typically require human intelligence, making it a versatile tool for organisations seeking to stay competitive in a rapidly evolving market. AI fosters collaboration between humans and machines, augmenting...

5 Partners

Melbourne, Sydney, Adelaide, Perth

Insights

The integration of AI into various sectors presents a unique blend of risks and opportunities that organisations must skillfully navigate. This section explores the dual nature of AI’s impact, focusing on the practical implications for business and society, offering a more pragmatic exploration of how AI reshapes industries and introduces...

5 Partners

Melbourne, Sydney, Adelaide, Perth

Partner with auditors you trust

Experience how structured, technology-driven audit services can strengthen your business. Our most recent case study displays real-world outcomes.