Insights

Say goodbye to leniency from the ATO. With harsher penalties for late lodgments and aggressive debt recovery tactics, now’s the time to engage proactively to avoid severe repercussions.

The good times are well and truly over, at least when it comes to dealing with the ATO. Whilst the ATO was largely understanding and supportive of taxpayers during the COVID pandemic, it’s fair to say that has come to an end, with increased activity on a number of fronts, including the imposition of penalties for late lodgments and a far tougher approach to debt recovery.

Penalty enforcements for Significant Global Entities (SGEs)

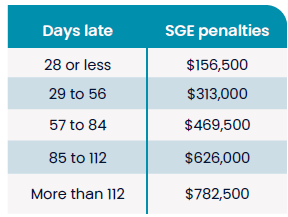

Broadly, an SGE is an entity that is part of a group with global turnover in excess of $1 billion. Whilst that is a very high threshold, it does nonetheless capture some relatively small Australian entities which are part of much larger global groups. As well as being subject to a host of additional regimes and lodgment requirements, SGEs are subject to very severe penalties for late lodgments of any tax related documents, with the current penalties being as follows.

These penalties are not new and have been a part of the SGE regime since its introduction in 2017. However, they were very rarely enforced and only so in cases of extreme non-compliance. That is no longer the case, with taxpayers starting to receive warnings as well as actual penalties for late lodgments. Whilst the ATO does typically give warnings before imposing the penalties, given the size of the penalties, it’s more important than ever to ensure timely compliance.

To stress the potential cost, the above are on a per document basis, so a taxpayer that has 3 activity statements outstanding for more than 112 days would be liable for a penalty of $2,347,500. The fact that there may be no debt associated with the activity statements is not relevant.

As a minimum, we recommend:

- Review Operations – all taxpayers with international operations should review their group’s operations to ensure they do not exceed the $1b threshold. We have seen many instances of taxpayers who were simply not aware of the fact they were an SGE.

- Ensure compliance - Taxpayers that are SGEs need to ensure that all their compliance obligations are up to date and engage early with the ATO if there are legitimate reasons that they expect to be late.

Debt recovery

Anyone that has had the misfortune of dealing with the ATO’s debt recovery teams recently will attest to the fact that they are a debt-recovery team first and ATO team second, with seemingly little consideration for ‘soft’ factors like employee welfare.

Resolving outstanding debt for the debt recovery team typically means one of two things:

- The debt is repaid in full.

- The company goes into liquidation.

Having said that, a lot can be done on the first point if taxpayers engage with the ATO in a timely manner. We have had great success negotiating very favourable payment plans with the ATO, but it does require early engagement and dialogue.

The ATO has itself reiterated this need for engagement, with a spokesperson noting the ATO’s “strong and deliberate action to deal with those who ignore their obligations and refuse to engage with us to pay their outstanding amounts”.

We recommend:

- Early Engagement: Engage with the ATO as soon as possible to negotiate payment plans and avoid more severe actions.

- Proactive Communication: Maintain open lines of communication with the ATO to demonstrate a willlingness to resolve outstanding debts.

26 Sept 2024

Related insights

Insights

As a result of COVID, the ATO went a little easier on taxpayers and suspended a lot of its compliance activities in 2020/21. These activities are now well and truly restarting and one of those is the Next 5,000 Tax Compliance Program.What is the Next 5,000 Program?Off the back of...

Boris Kresic

Partner

Sydney, Newcastle

Insights

Under legislative changes, Discretionary Trusts that own residential land in NSW and which do not specifically exclude foreign persons (as defined) as beneficiaries, will be subject to surcharge Land Tax. Such trusts have until 31 December 2020 to amend their Trust Deed. Therefore, where a Discretionary Trust is the owner...

Boris Kresic

Partner

Sydney, Newcastle

Insights

Taxation in Australia is both complicated and constantly changing. Public interest in the tax system is arguably at an all-time high. Politically there is a desire to increase tax transparency for larger businesses and high net worth individuals to provide community confidence that ‘the bigger end of town’ is paying...

Garry Mathoda

Partner

Sydney