Insights

PKF Wealth and Newlane Risk enter into a new JV to bring a new level of service for PKF Wealth clients. Daniel Isenhood I Personal Insurance Adviser I PKF Wealth I Sydney and Newcastle

In May of this year, PKF Wealth established a joint venture with Newlane Risk. This strategic partnership enables the PKF Wealth Adviser Team to exclusively focus on wealth creation and retirement funding solutions, while Newlane Risk is committed to enhancing the quality of PKF’s advisory services in Personal Insurance, particularly the provision of Life and Disablement insurance.

Wealth and retirement planning have undergone rapid transformation in every aspect. Significant challenges have risen from the advancement of technology, including the consequences of A.I., the increasing whitenoise of ESG and cryptocurrency, and the need to adapt to regulatory changes.

Keeping up with the speed of wealth markets and packaging it for client consumption is a specialisation. Separately, the other specialisation within financial advice is obtaining, maintaining and claiming personal insurance.

Over the last six years the insurance industry has seen evolved immensely. Unlike the excitement of wealth, the forces of change within insurance are driven primarly by claims. Very successful claims.

In 2022 alone, Zurich, which includes their OnePath product range, paid claims to Australians, across all product lines in excess of $1.3B. TAL paid $3.5B in claims to Australians. While AIA paid $2.1B.

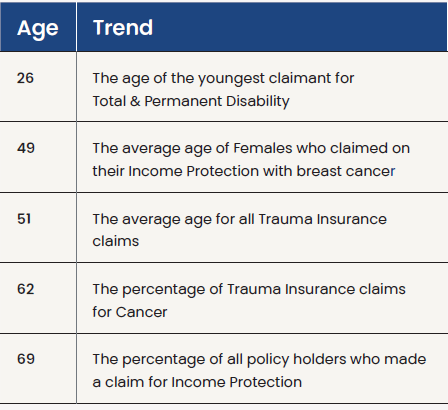

Claim trends across the three major insurers is similar. These are worth highlighting:

This is in part reflective of Australia’s generous policy designs colliding with our aging population, a significant uptick in middle-age metastsies, auto-immune diseases and poor mental health.

Once again, insurance’s opposing forces need to be reconciled. There is no doubt the eye watering sums paid in the form of claims is heartening. However, insurance companies and their regulator APRA insist that sustainability and viability must be maintained.

For insurers to absorb claims growth they must share the burden with customers and their advocates (us advisers).

Insurance companies are limited to very few strategies to counter claim growth plus achieve sustainability and they are fundamental to your policy ownership. These strategies are:

OBTAIN - Conservative selection or greater discrimination at time of underwriting.

- The best time to obtain insurance is while you’re healthy. Attempting to time the purchase of insurance just prior to lifes hazards is like trying to catch a falling knife by the handle.

- Life is neither neat nor predictable and health challenges can’t be avoided, therefore its essential we find the right insurer to meet your unique risks.

Once again, insurance’s opposing forces need to be reconciled. There is no doubt the eye watering sums paid in the form of claims is heartening.

MAINTAIN - Adjusting premiums upwards. Age-based premiums increase yearly. Additionally, if claims experience is excessive, insurers will further increase premiums across their pool of risk. This can put frustrating pressure on any family budget.

- Proactive premium management strategies is a fundamental of overall risk management.

CLAIM – All Australian retail insurers have worked very hard for their market positions and brands and are loathe to make the claim process any harder at such a trying time.

- No insurer is perfect, which makes our role as a claim advocate crucial for an expedient successful outcome.

Furthermore, claim success in 2023 is stronger than ever before due to strong regulatory decision-making and insurers sustainable strategies. Personal insurance has never been more important to Australian families and businesses.

Newlane’s objective is to help PKF Wealth clients navigate all facets of policy ownership. If you’d like to explore a review of your insurance needs or if you’d simply like a reminder of your existing arrangements, please get in touch with us directly or ask your PKF Tax or Wealth Adviser for an introduction.

4 Oct 2023

Author

Daniel Isenhood

Personal Insurance Adviser

Sydney and Newcastle