Insights

The landscape of anti-avoidance measures is evolving as the ATO’s focus intensifies, demanding vigilant consideration of trust arrangements and income distribution strategies Boris Kresic I Partner I Sydney Taxation

Section 100A is an anti-avoidance provision. Although it was enacted in 1979, it has recently become one of the ATO’s key focus areas. The typical target scenario is when a trust makes a beneficiary on a lower tax rate presently entitled to income, but the underlying economic benefit is received by another beneficiary (on a higher tax rate).

Where section 100A applies, the trustee will be assessed at the top marginal tax rate.

Recent ATO views

On 8 December 2022, the ATO released its final guidance on section 100A in the form of:

- Taxation Ruling TR 2022/4

- Practical Compliance Guideline PCG 2022/2

The ruling and PCG cover various scenarios and also set out a traffic light system for the application of compliance resources. However, the biggest change is arguably the way in which the ATO will seek to apply the ordinary family dealing exception.

Broadly, where an arrangement is seen as an ordinary family dealing, section 100A cannot apply. Historically, many taxpayers have taken the view that making a family member presently entitled to trust income whilst giving the financial benefit to another member is an ordinary family dealing and therefore outside the scope of section 100A. The ATO guidance now makes it clear that this would generally not be the case, except in the case of spouses.

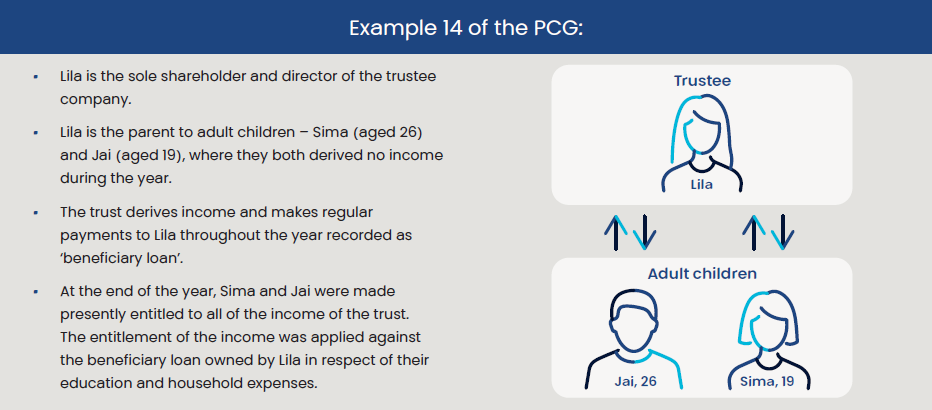

A typical arrangement that would attract attention can be demonstrated in example 14 of the PCG:

Recent case law

To further complicate matters, on 24 January 2023 (after the ATO issued its guidance), the Full Federal Court handed down its anticipated decision in Commissioner of Taxation v Guardian AIT Pty Ltd ATF Australian Investment Trust (Guardian). Although the case involved a somewhat unique set of facts, the Commissioner lost in relation to the application of section 100A. The case therefore poses some real question marks about the validity of the views expressed by the ATO in its recent ruling and PCG and the ATO recently stated in their Decision Impact Statement that minor updates will be made to TR 2022/4 to reflect aspects of the Court’s decision.

Key takeaways

TR 2022/4 and PCG 2022/2 apply both prospectively and retrospectively with no time limit of amendment of assessments. However, in most cases, the ATO will only apply section 100A within four years of the trustee lodging the tax return. The ATO will not review arrangements prior to 1 July 2014, other than in exceptional circumstances as outlined in the PCG.

For anyone that falls outside the areas of safety, particularly with arrangements where an adult child with a lower tax rate is not receiving the underlying benefit of their distribution, please contact your PKF adviser for further guidance.

For more information on section 100A, please contact Boris Kresic from your PKF tax team.

4 Oct 2023