Insights

Time Horizon Investment strategy mitigates sequencing risk by aligning short, medium, and long-term portfolios to ensure steady cash flow in retirement.

The question advisers are most often asked is “will I have enough money to retire comfortably?”. While the answer to this question depends on a number of different factors, a key element that determines the outcome can come down to market conditions at the time of retirement.

Unfavourable market conditions just before or at the beginning of someone’s retirement phase of their life can significantly impact the longevity of retirement savings. The issue being investors have a limited time to recover and no income to replace the lost savings. This is called sequencing risk and in short, a poor sequence of returns leads to poor outcomes.

In order to mitigate the effects of sequencing risk, we can employ a Time Horizon Investment (THI) strategy. This strategy aims to build a client portfolio that considers future spending needs and wants over a particular time frame. Typically, the needs are calculated for the short, medium and long term, and then we determine the asset allocation using several portfolios that are most appropriate to fund cashflow requirements.

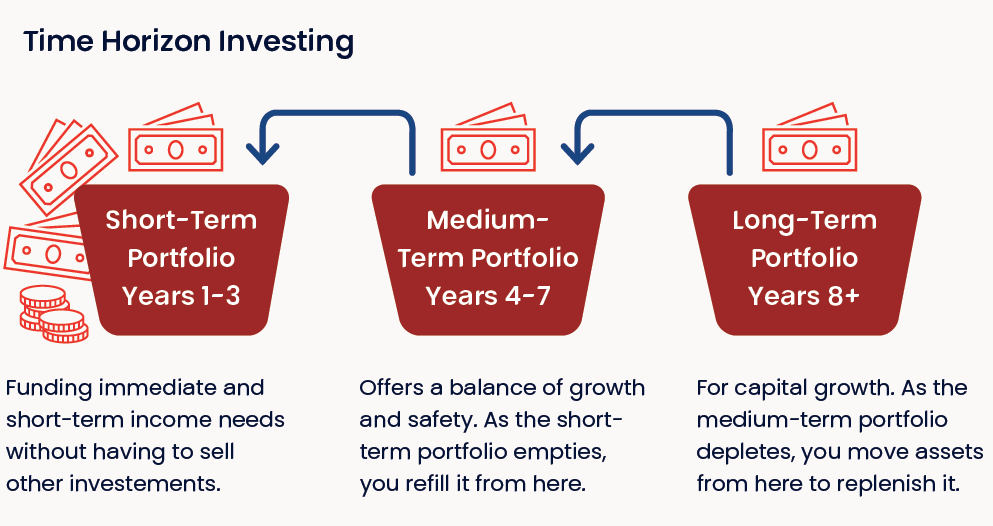

Fundamentally, the THI strategy has three portfolios, or ‘buckets’ of wealth - short term, medium term, and long term.

Short term: The short-term bucket is to fund the next three years of cash needs. This bucket will be allocated to low-volatility, low-risk investments such as cash and fixed interest bonds.

Medium term: The medium-term bucket is used to fund cashflow needs for the next following four to seven years. This bucket has exposure to growth assets (international and domestic equities, property, infrastructure) and defensive assets (cash and fixed interest).

Long term: The long-term bucket is used primarily to drive returns for the overall portfolio and uses these returns to top up the short and medium-term buckets as funds are being withdrawn to enjoy retirement.

Regular reviews are crucial for the ongoing success of the strategy to ensure each bucket remains appropriately weighted. Where market returns have been generally positive, the medium, and long-term buckets will cash in on some of the gains and top up the short-term bucket and restore the allocations at the strategy inception. Where markets have been generally negative, rebalancing of portfolios is deferred, and the client can rest easy knowing their cashflow needs for the next three years are funded allowing markets have an opportunity to recover.

Naturally, this is not a ‘one size fits all’ strategy. However, it is very effective at mitigating the sequencing risk for those it is suitable. Having a strong understanding of cashflow needs in the short and medium-term is instrumental to the success of the strategy for clients and advisers alike.

6 Mar 2025

Related insights

Insights

Following the initial rollout of Pillar Two rules in Australia, the Australian Taxation Office (ATO) has now released further guidance detailing the lodging, payment, and compliance obligations for multinational enterprise (MNE) groups under the Global Anti-Base Erosion (GloBE) framework.

Becky Nguyen

Partner

Melbourne

Insights

随着2024–25财年即将结束,个人纳税人迎来了一个关键时机,可通过审视自身的收入状况、养老金缴款、投资活动及可扣除项目,高效管理税务事务。由于重大个税税率调整将自2024年7月1日起生效,现阶段具备优化税务结构的空间——但相关安排必须在6月30日之前完成。

Ryan Lu

Partner

Melbourne

Insights

As the end of the 2024–25 financial year approaches, individuals have a crucial opportunity to review their income position, superannuation contributions, investments, and deductions to manage their tax affairs efficiently. With significant changes to personal income tax rates taking effect from 1 July 2024, there is scope for tax optimisation, but action must be taken before 30 June.

Ryan Lu

Partner

Melbourne