Insights

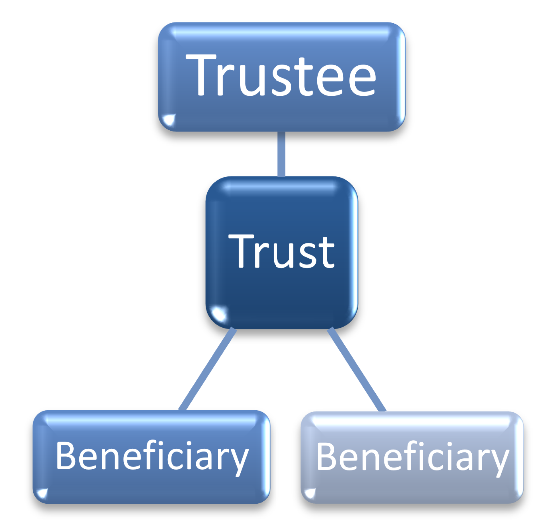

What is a Trust?

A trust is NOT a separate legal entity; it is a relationship.

It does not pay taxes (however, DOES require lodgement of a separate income tax return) nor can it hold title over any assets. It is a vehicle in which assets are held by a legal trustee for its beneficiaries.

The two main kinds of trusts are:

Unit Trusts - the beneficiaries have a proportionate entitlement to the assets of the trust and any profits from them are determined by the amount of units held and

- Discretionary Trusts – the beneficiaries each year are determined at the discretion of the trustee.

- Discretionary Trusts can make elections to become Family Trusts, which then limits the range of potential beneficiaries to the family group and any interposed entities.

Why did Trusts come into existence?

To over-simplify it: ‘back in the day’, there were some who could not legally own land or have land passed down to them – widows, daughters, younger sons, illegitimate children, This posed a problem if say a husband were ill and wanted his wife to be able to continue living in their family home after his death.

Since he could not leave the property under the ownership of his wife, the alternative was to leave the legal ownership to another male (say, his brother) whom he ‘trusted’ to take care of the legal ownership of the asset while ensuring all ‘benefits’ remained with the wife.

In this situation, the brother is the Trustee, the house is the asset of the Trust and the wife is the Beneficiary. The husband is the Settlor (the one who has settled the trust over the asset and dictated his wishes to the trustee, generally in a written deed).

How does a Trust work?

Since a trust is not a separate legal entity, it cannot retain profits in the way that a company can. Each year the trustee must resolve to distribute any profits to the beneficiaries; on which they then pay tax in their own names. If the trustee does not allocate the income to beneficiaries appropriately, the trustee will be assessed at the highest marginal tax rate (currently 47%).

The trustee must be a separate legal entity – either individual(s) or a company.

What are some tricks and traps?

Trustee distribution resolutions must be in place by 30 June of each year (subject to provisions of the deed). This makes tax planning very important.

Clients (and other contacts like bankers etc) often confuse the trustee and the trust e.g. XYZ Pty Limited ATF ABC Trust – they may phone and ask you about XYZ Pty Limited when they really mean the trust.

Trust deeds are unique and specific to each trust – you must review each trust deed in all cases.

How does it relate to the work we do for our clients?

A lot of our clients have one or more trusts as part of their group structure. This means we must be aware of the functionality and tax provisions around trusts e.g. to prepare their year end compliance work.

As part of any tax planning work we do, we must consider trusts, including preparation of the trustee distribution resolutions prior to 30 June.

We must be aware of the benefits and potential pitfalls of trusts as part of any structuring / restructuring work.

For more information

5 May 2025

Related insights

Insights

What is Superannuation? Superannuation is cash set aside over your lifetime to assist in funding your retirement. It generally cannot be accessed until you reach an eligible age, however hardship provisions may allow early access. What are Superannuation Funds? There are two types – public offer (e.g. industry funds) and...

Stacie Shaw

Partner

Newcastle, Sydney

Insights

What is PAYG? Pay-As-You-Go requires tax payments as income is earned (not just on lodgement of an income tax return); imposed as Withholding and Instalments. PAYGW is withheld by the payer and they remit it to the ATO (e.g. employers remit on behalf of employees; banks remit on behalf of...

Stacie Shaw

Partner

Newcastle, Sydney

Insights

What is Fringe Benefits Tax (FBT)? FBT is a tax that ‘catches’ benefits provided to employees that don’t have tax withheld from them the way wages normally would. Why was FBT imposed by the ATO? Employees got ‘cute’ about saying to their employer: “Rather than pay me wages, which you...

Stacie Shaw

Partner

Newcastle, Sydney