Insights

Division 296 proposes a 15% tax on super balances over $3m, but it’s only on the earnings above this threshold, not the entire balance increase.

From 1 July 2025, the Government has proposed a new tax on those who have a total superannuation balance (TSB) of greater than $3 million. The new tax is called Division 296 (Div 296) and the proposal is for an additional 15% tax to be levied on the movement between a member’s opening and closing TSB for the year. This movement is referred to as the 'earnings' amount.

Some of the key points about this proposed legislation that are often misunderstood:

- There is no instant tax payment for balances over $3m. The earnings calculation is only interested in the movement of a member’s balance from one year to the next i.e. from 1 July 2025 to 30 June 2026.

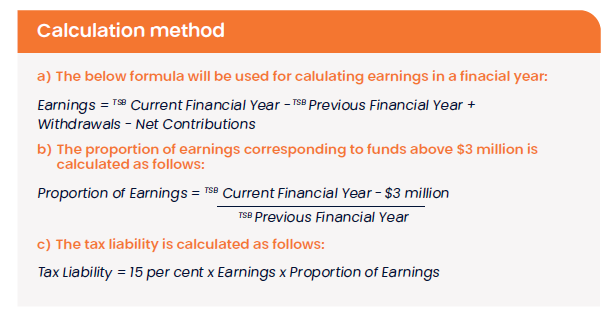

- It is not a flat 15% tax on the increase of a member’s balance. It is only on the proportion of your balance that is over $3m on 30 June. This means that the effective tax rate will always be less than 15% as can be seen in the below calculation method:

- If legislated, the first payment of the new tax will not be due until the 2027 financial year.

- There is no change to how the current tax system works for an SMSF. This is an additional stand-alone tax.

It is important to remember that Div 296 tax is not yet law and could change before being finalised. It is also worth noting that the Shadow Assistant Treasurer Luke Howarth recently remarked that the Coalition would reverse the proposed Div 296 tax if it won the next election.

There are numerous organisations including the SMSF Association that continue to strongly oppose the legislation and its design. The main points of contention are:

- Unrealised gains should not be counted as taxable superannuation earnings;

- If unrealised gains are taxed, then a loss carry back or refund system should apply as the proposed carry forward loss approach will result in tax being paid on unrealised gains that may later result in a loss; and

- The $3 million threshold should be indexed.

For most circumstances, superannuation is still the most tax effective structure. When considering the effects of the proposed Div 296 tax, individuals should work with their accountants and advisors to ensure the best outcome for their specific situation.

26 Sept 2024

Related insights

Insights

With increased scrutiny on SMSF property valuations, trustees

must ensure valuations are based on objective, supportable data

and meet updated guidelines to avoid audit complications.

Daniel Clements

Partner

Newcastle, Sydney

Insights

Setting up a Self-Managed Superannuation Fund (SMSF) requires careful planning and adherence to regulatory requirements. Here’s a checklist to guide you through the process: Pre-setup considerations 1. Research and education Understand the roles and responsibilities of SMSF trustees. Educate yourself about SMSF regulations, investment options, and taxation implications.There are various...

Daniel Clements

Partner

Newcastle, Sydney

Insights

A common misconception about death and your Self Managed Superannuation Fund (SMSF) is that your super entitlements are automatically dealt with as part of your estate or will. This is not the case! Your superannuation may be a significant asset when you die and it should be carefully considered in...

Daniel Clements

Partner

Newcastle, Sydney